I’ve written a lot about how to pay for your wedding – including how to create a budget, whether or not to incur debt, tracking expenses, etc. Well, today I’m writing a case study about how Luis and I paid for our wedding – including our actual numbers. In this article, you’ll learn the exact steps we took to figure out how to pay for our wedding and the strategies behind our decisions.

Starting Our Wedding Fund

We got engaged in January 2016 and soon after our engagement high, we came back to reality and talked about how we would pay for the wedding.

We considered funds that we could potentially use to fund our wedding:

- Financial support from family: We crossed this off of our list immediately because we were planning to pay for the entire wedding ourselves, so this resource wasn’t available (though my mom ended up paying for half of my dress, and his mom ended up purchasing the wedding favors)

- Credit card rewards: I had been using a travel rewards credit card and I had a pretty large accumulation of points. So we agreed to use that towards our honeymoon. We also agreed to pay as much of our wedding expenses with my credit card to earn even more points for the honeymoon.

- Savings: We each had some savings, and we committed to contribute $1,500 each toward the wedding – so we started out with $3,000 total.

Our First Joint Bank Account

Soon after we decided how much to contribute towards the wedding, we decided to open up our first joint bank account – which we used specifically to pool our wedding funds. When we opened up our wedding bank account, our initial deposits were $1,500 each and we continued to fund the account each month with funds from regular monthly paychecks.

Monthly Contributions: How Much?

This is the fun part! Most of our wedding was funded by consistent contributions from our monthly cash flow. So we each had to take a look at our monthly budgets and figure out how much we could contribute consistently each month. After reviewing everything, we each agreed to contribute $500/month. In total between the two of us, that was a total of $1,000/month.

Monthly Contributions: For How Long?

Next, we had to figure out how many months we were we willing to make these monthly contributions. I said I didn’t feel like making these monthly contributions for more than 24 months* and Luis agreed. That was easy! So we committed to making our monthly wedding contributions for exactly 24 months.

*How Did I Come Up With 24 Months?

The simple answer to this question is that I just didn’t feel like spending more than two years of our lives paying for a one-day event; two years was my absolute maximum. And I know two years still sounds like a long time to pay for a wedding, but here’s what I figured:

- We could save up for one year BEFORE the wedding – because most weddings take about one year of planning

- We could continue making contributions for one year AFTER the wedding – if we took on some debt, we could pay it off within a year of our wedding day. That sounded like a realistic goal that wouldn’t feel so burdensome, so the idea of wedding debt didn’t sound so bad after all.

And by the way, the main reason we agreed to incur wedding debt was because I just didn’t want to wait two whole years to get married! I didn’t want to put our wedding on hold if we didn’t have to. And thanks to my zero-interest balance transfer, we didn’t have to postpone our wedding!

Putting It All Together: Our Wedding Budget

At this point, we had enough information to come up with our wedding budget (i.e. how much wedding we could afford). We knew how much we could contribute each month ($1000/month) and how long we planned to contribute that amount (24 months). We did some simple math ($1000/month * 24 months) and we found that our (shared) wedding budget was set at a total of $24,000.

This ended up being our shared wedding budget, which means there were a few items that we chose to pay for with our own separate money. I started that trend when I mentioned to Luis that I would pay for my wedding dress out of my own pocket because I didn’t want my wedding dress price to be restricted by our shared wedding budget. Luis shared my logic and he decided to pay for his attire on his own too.

Things Don’t Always Go According to Plan

If you can’t already tell, I’m a planner when it comes to personal finances. I always like to have a plan in place, but I know that things can change – and that’s ok! I think it’s important to be open to changes, and make adjustments as necessary to keep moving forward.

For example, Our initial plan to contribute $1000/month quickly turned. Luis and I initially agreed to contribute $500/month each. But a few months in, Luis realized that this wasn’t sustainable for him after all. So he reduced his monthly contribution down to $400/month. But the cash we contributed upfront ended up covering the loss of $100/month – phew! Luckily, Luis’ reduced monthly contribution didn’t set us back on our goals; we were still on track with our original budget of $24,000.

Wedding Debt

As I’ve mentioned before, we incurred some wedding debt. I know wedding debt gets a bad rap – but for us, it made total sense and everything turned out fine.

We got engaged in January 2016 and we get married in March 2017. By the time we got married, we had saved up $15,000 in the bank, and we only needed to borrow $9,000 to fund our $24,000 budget.

Even though we could have easily borrowed well over $9,000, we decided to stick to our budget and our plan. We didn’t borrow a penny more than we needed – because we already had a debt payoff plan in place. It took a lot of discipline, but I’m glad we stuck to our original plan.

Staying Motivated to Pay Off the Debt

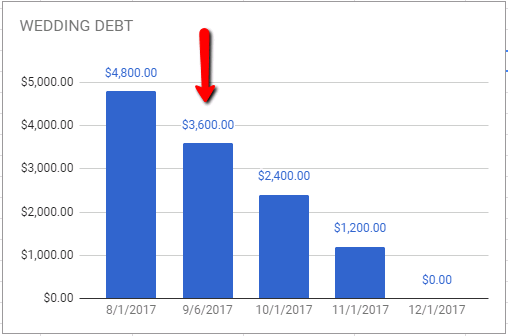

Luis and I planed to make our monthly contributions for 24 months straight. And that’s what we did. After the wedding – instead of depositing our contributions in the bank, we paid those contributions towards the wedding debt. So even though our minimum payment on the debt was around $25/month – we paid more more than the minimum. This helped us stay on track to meet our goal.

Another strategy that helped us payoff the debt quickly was our zero-interest balance transfer. We didn’t pay a dime of interest on our $9,000 balance because we took advantage of a balance transfer offer.

Also, as we were paying off our debt, I’d send out a monthly update after each payment. These updates were a great visual reminder of our progress. And look at how adorable these graphs are!

Mission Accomplished!

When we paid off our wedding debt, we felt SO accomplished! We worked as a team, we committed to the debt payoff plan, and we came through on our first financial goal as a married couple! Plus, our careful planning and success set a positive vibe for our future financial journey together.

Leave a Reply